|

|

Home >Country Analysis Briefs>Arab Maghreb Union |

|

|

Home >Country Analysis Briefs>Arab Maghreb Union |

|

|

|

Page Links |

January

2002

Arab Maghreb Union The Arab Maghreb Union (AMU), which includes Algeria, Mauritania, Morocco, and Tunisia (plus Libya, covered in a separate report ), is an important oil and gas producer, exporter, and transit center (to southern Europe). Natural gas production from the region is increasing, and new pipelines to Spain and Italy are being planned. Note: Information contained in this report is the best available as of January 2002 and is subject to change.

Given the decline in oil prices in recent months, however, these positive trends are beginning to show signs of reversing, with a significant budget deficit, for instance, now expected in 2002. Continued economic, social, and political problems for Algeria include: high unemployment (around 30%, and apparently rising); continued political violence by Islamic fundamentalists and others (including several bomb attacks on Algiers during Ramadan); labor unrest; a large black market (possibly 20% of the country's GDP); continued weakness in the non-oil economy (a severe drought hurt the agricultural sector in 2000, and massive flooding struck northern Algeria in November 2001, killing 800 and causing an estimated $300 million in damage); slow progress on economic reform efforts (largely due to opposition by labor unions and the armed forces); and protests by a restive Berber minority demanding greater autonomy, increased employment opportunities, and better living conditions. Algeria remains highly dependent on oil and natural gas exports, which account for more than 90% of Algerian export earnings, and about 30% of GDP. In early January 2002, Algeria adopted a $19.1 billion budget for 2002, based on an assumption of $22 per barrel for Algerian oil. In December 2001, the International Monetary Fund (IMF) issued its annual "Article IV" assessment of the Algerian economy, urging that the government proceed with privatization and banking reform, while lowering tariffs aimed at protecting domestic industry and reducing dependence on hydrocarbons. The IMF praised the Algerian government for its strong fiscal discipline (and careful monetary policy as well), and for allowing the dinar to depreciate against the dollar. Finally, the IMF pointed out that high oil prices provide Algeria with an opportunity to make progress on implementing reforms and addressing the country's many problems. In 2001, Algeria's privatization program continued to move ahead, despite the firing of the country's privatization minister, Hamid Tenmar, and with largest state companies (including those in the energy sector) mainly still in state hands. In late 2001, an important new hydrocarbons law moved ahead, with passage possible in early 2002. This law would open Algeria's all-important energy sector to private (including foreign) investment, although state oil and gas company Sonatrach would most likely remain in public hands. The law faces opposition from labor unions, and already has been watered down somewhat from its original form. President Abdelaziz Bouteflika, elected President on April 15, 1999 for a 5-year term, has attempted to implement plans for national reconciliation and economic reforms (i.e., deregulation, privatization). More than 100,000 rebels, soldiers and civilians have died in Algeria's civil war, which began in 1992 following the military's nullification of a national election won by the Islamic Salvation Party. On July 13, 1999, President Bouteflika offered amnesty to rebel groups, and on September 16 a national referendum was held in which voters approved the offer. Although the government claimed that nearly 80% of rebels (including members of the Islamic Salvation Army) accepted amnesty, the level of violence appeared to rise once again, with the most violent groups apparently stepping up attacks. In August 2000, President Bouteflika replaced Prime Minister Ahmed Benbitour with Ali Benflis. The next parliamentary elections are scheduled for June 2002. In July 2001, President Bouteflika visited the United States and met with President Bush. Oil

Official estimates of Algeria's proven oil reserves remain at 9.2 billion barrels. With recent oil discoveries, plans for more exploration drilling, improved data on existing fields, and use of enhanced oil recovery (EOR) systems, proven oil reserve estimates are expected to be revised upward in coming years. Algeria should also see a sharp increase in crude oil exports over the next few years due to a rapid shift towards domestic natural gas consumption and planned increases in oil production by Sonatrach and its foreign partners. Approximately 90% of Algeria's crude oil exports go to Western Europe, with Italy as the main market followed by Germany and France. The Netherlands, Spain and Britain are other important European markets. Algeria's Saharan Blend oil, 45o API with 0.05% sulfur and negligible metal content, is among the best in the world. Algeria's Minister of Energy, Chekib Khelil, recently indicated that the government is considering restructuring the state oil company, Sonatrach (and Sonelgaz, the state utility) in order to attract private international investment. The major impending change Khelil outlined was to have the Energy Ministry take on Sonatrach's regulatory and negotiating roles. Sonatrach would remain the national oil company but eventually would be forced to compete for new projects. Khelil also raised the idea of privatizing non-core subsidiaries of Sonatrach, in the context of discussing the government's broader privatization efforts - which extend to banks and utilities. It is believed that new legislation now pending would help these state corporations attract foreign investment. Oil Production By far, the largest oil field in Algeria is Hassi Messaoud, located in the center of the country, which produces about 400,000 bbl/d of 46o API crude, down from 550,000 bbl/d in the 1970s, but up from 300,000 bbl/d in 1989. The Hassi Messaoud area contains an estimated 6.4 billion barrels, or about 70% of the country's proven oil reserves. Sonatrach operates Algeria's other major oil fields, including Rhourde el-Baguel (Algeria's second largest oil field, located to the northeast of Hassi Messaoud), Tin Fouye Tabankort Ordo, Zarzaitine (30,000 bbl/d), Haoud Berkaoui/Ben Kahla, el-Gassi el-Agreb and Ait Kheir. The Hassi R'Mel gas field (north of Hassi Messaoud, south of Algiers) also produces around 18,000 bbl/d of 46.1o API crude. In April 2000, Amerada Hess announced that it had acquired (for $55 million) the Gassi el-Agreb Redevelopment Project from Sonatrach. Amerada Hess will form a joint operating company with Sonatrach, to be called Sonahess, and will invest $500 million over 5 years to enhance recovery from the el-Gassi, el-Agreb, and Zotti fields. Currently, the three fields produce around 30,000 bbl/d, and the redevelopment project aims to increase production to 45,000 bbl/d by late 2003. Algeria's oil sector, unlike that of most OPEC producers, has been open to foreign investors for more than a decade. One of the largest joint ventures in Algeria is the partnership between Anadarko, Lasmo and Denmark's Maersk Oile to develop the Hassi Berkine South oil field. Oil from the field's Block 404 was first produced in May 1998; the field was producing approximately 74,000 bbl/d as of September 2001. It is estimated that production at the field will increase to 135,000 bbl/d following completion of a second oil production train on September 5, 2001. Production then could double once again as two additional, 75,000-bbl/d trains are completed (possibly by September 2002) to process oil from Blocks 403 (Agip/Sonatrach) and 404 (Anadarko/Sonatrach). BHP has stated that it will spend $190 million on oil field development at the "ROD" integrated oil development project in the Berkine Basin in eastern Algeria. Production is expected to commence in 2003, and peak at 80,000 bbl/d. Also in June 2000, First Calgary Petroleums Ltd. announced that it would explore Block 406a (Rhourde Yacoub) in Berkine, and in July 2000, several companies (Burlington Resources, Talisman, and Sonatrach) announced that they would develop the MLN field in Block 405a. MLN is expected to produce around 35,000-40,000 bbl/d when completed. Exploration success rates in the Berkine Basin have been high, and several billion barrels of oil may lie within 15 miles or so of the area. Spain's CEPSA has announced a $1.3-billion plan to develop its 1-billion barrel Ourhoud oil field in conjunction with Sonatrach. The field, which is slated for eventual production of 230,000 bbl/d, is divided into three blocks operated by Anadarko, Cepsa, and Burlington Resources. Work on a 500,000-b/d oil pipeline to service the field already has been completed by an Anadarko-led consortium. Although Algeria has experienced a significant influx of foreign investment in recent years, it still has many oil fields in need of additional foreign capital and EOR investment. Halliburton has an eight-year contract to provide EOR services and boost production at Hassi Messaoud, for instance, which saw production fall sharply beginning in the mid-1980s. Algeria's second largest oil field, Rhourde El Baguel, has already received foreign investment to boost its production capacity. Rhourde El Baguel contains about three billion barrels of 42.6o API oil, of which less than 450 million barrels has been produced since 1963. In February 1996, Arco (now owned by BP) signed a $1.3-billion production sharing agreement (PSA) with Sonatrach to increase production at the field. BP expects to raise the field's output from 27,000 bbl/d to 125,000 bbl/d by 2010. In early October 2001, Sonatrach awarded five new exploration contracts -- all in the Berkine basin -- as part of Algeria's second licensing round. Companies receiving blocks included Anadarko (406b), Burlington Resources (402d), First Calgary Petroleum (406b), TotalFinaElf (432, 444s, 403n), and Repsol-YPF (401d), all currently active in Algeria. Also, in November, a tender for development of five oil and natural gas projects in the Illizi Basin received 14 bids from foreign companies such as BP, TotalFinaElf, Amerada Hess, and BHP Billiton. Besides Illizi itself, projects include Zarzaitine, El Adeb Larache, Rhourde Nouss, Tinrhert. Two other companies working in the Illizi basin include Ireland's Tullow Oil and Japan's Teikoku Oil (Block 222b). Downstream Although Algeria has a substantial petrochemical and fertilizer industry, low capacity utilization rates mean continued reliance on imports. The majority of Algeria's petrochemical plants are located at Annaba (a 550,000-ton- per-year (t/y) - ammonium phosphate fertilizer plant and ammonium nitrate and nitric acid complex), Arzew (365,000 t/y ammonia, 146,000 t/y urea, and 182,500 t/y ammonium nitrate), and Skikda (a 130,000 t/y high-density polyethylene unit, 120,000-t/y ethylene cracker, and a substantial aromatics complex). Sonatrach has undertaken a number of petrochemical and fertilizer expansion projects, including a new methyl tertiary butyl ether (MTBE) complex and a polyester resin complex. Algeria has seven coastal terminals for crude oil, refined product, NGL, and liquefied natural gas (LNG) exports. These are located at Algiers, Annaba, Arzew, Bejaia, Oran, Skikda, and La Skhirra. Arzew handles about 40% of Algeria's total hydrocarbon exports (including all of its NGL exports), and Algeria has ambitious plans for the port area. Among other things, the government would like to build a petrochemicals complex at Arzew, as well as a condensate refinery and desalination plant. Work also needs to be done to maintain and upgrade Arzew's crude oil loading capacity. A refurbishment project on the port began in 1998. Besides Arzew, Algeria uses the Tunisian port of La Skhirra exclusively for crude exports. Natural Gas Algeria's largest gas field is the super-giant Hassi R'Mel, which initially held proven reserves of about 85 Tcf. Hassi R'Mel accounts for around 1.35 billion cubic feet (Bcf) per day, or about a quarter of Algeria's total dry gas production. The remainder of Algeria's gas reserves are located in associated and non-associated fields in the southeast, and in non-associated reservoirs in the In Salah region of southern Algeria. The Rhourde Nouss region holds 13 Tcf of known reserves in the Rhourde Nouss, Rhourde Nouss Sud-Est, Rhourde Adra, Rhourde Chouff, and Rhourde Hamra fields. Smaller gas reserves are located in the In Salah region (5-10 Tcf) as well as at the Tin Fouye Tabankort (TFT)(5.1 Tcf), Alrar (4.7 Tcf), Ouan Dimeta (1.8 Tcf), and Oued Noumer fields. Four plants at Arzew and Skikda, owned by Sonatrach, liquefy gas for export. Algeria's natural gas pipeline export capacity includes 850 Bcf/y via the 667-mile Trans-Mediterranean (Transmed, renamed Enrico Mattei) line from Hassi R'Mel via Tunisia and Sicily to mainland Italy, and 285 Bcf/y via the 1,013-mile Maghreb-Europe Gas (MEG, renamed Pedro Duran Farell) line via Morocco to Cordoba, Spain, where it ties into the Spanish and Portugese gas transmission networks. With EU natural gas demand growing rapidly, Algeria has plans to increase its natural gas export capacity significantly in coming years. In August 2001, Sonatrach awarded ABB a $93 million contract to build a natural gas compressor station on the Pedro Duran Farrell (MEG) line in order to raise capacity to 390 Bcf/y. (Note: ABB also was awarded a $70 million contract in June 2001 to upgrade an oil pipeline between Hassi Berkine and Haoud El Hamra). In late July 2001, Spain and Algeria agreed to move ahead with a new natural gas pipeline (Medgaz) linking Algeria directly to Europe via Spain. TotalFinaElf, along with Sonatrach and Spain's Cepsa, previously had agreed (in October 2000) to study the line's feasibility (since then, several other companies -- Endesa, Gaz de France, and TotalFinaElf -- have acquired shares in Medgaz). The 350-530 Bcf/y Medgaz pipeline most likely would go from Hassi R'Mel through the port of Arzew to Almeira, Spain. Also, in December 2001, Sonatrach signed a deal with Italy's Enel and Germany's Wintershall on a feasibility study of yet another new natural gas pipeline, this one from Algeria under the Mediterranean Sea to Sicily and onwards to the Italian mainland and also southern France. Aside from exports to Italy, Spain, etc., Algeria has a policy of using its natural gas reserves as a source of domestic energy and as a raw material for the petrochemical industry. Approximately 95% of the country's electricity is generated by natural gas. Development of the In Salah region is one of the lynchpins in Algeria's plan to increase its natural gas exports. In February 2000, BP Amoco and Sonatrach signed a $2.5-billion deal to develop seven of the twelve existing fields in the In Salah region, including the Garat al-Bafinat, Teguentour, Krechta, Reg, In Salah, Hassi Moumeme, and Gour Mahmoud fields. These fields contain estimated dry natural gas reserves of 5 Tcf, with a potential for 10 Tcf total. In addition, the joint venture, called In Salah Gas, will appraise existing wells and explore for new gas reserves in the In Salah region. In Salah Gas is the first major natural gas joint venture between Sonatrach and a foreign partner. Production from the region originally was expected to come online in late 2003, after the drilling of up to 200 production wells and construction of a $1-billion, 48-inch pipeline link to Hassi R'Mel. However, progress has been slowed due to several factors, including EU rules on natural gas re-exports and slow natural gas demand growth in potential importing countries such as Spain, and production now is expected to begin in 2004. Main engineering work on In Salah is to be performed by Japan's JGC; U.S.-based Kellogg, Brown, and Root; Bechtel; and Sonatrach subsidiary Enefor. In May 1997, In Salah Gas sealed its first natural gas sales deal with Italian electricity generator Enel. The deal enables In Salah Gas to take over an existing contract to supply Enel with 141 Bcf/y of gas. Sonatrach will continue supplying the Italian power giant with natural gas supplies until In Salah is ready. The deal represents In Salah's first step towards achieving its sales goal of 318-388 Bcf/y. Besides Enel, the venture is also marketing gas to other potential clients in Europe, Turkey and North Africa. Besides In Salah, two other important Algerian natural gas and condensates projects are Ohanet and In Amenas. Ohanet is located in the Illizi province on the northern edge of the Sahara desert about 60 miles west of the Libyan border. Ohanet is being developed -- at a cost of $1 billion -- by Australia's BHP (with a 45% share), Woodside Petroleum (15%), Japan Ohanet Oil and Gas, Swiss-Swedish ABB, and U.S.-based Petrofac. Production from Ohanet is expected to begin in 2004, and is to include natural gas, natural gas liquids, and liquefied petroleum gas (LPG). The development project includes construction of a natural gas processing plant, with capacity of 30,400 bbl/d of condensate, 27,700 bbl/d of LPG, and 665 million cubic feet (Mmcf)/day of natural gas -- as well as a pipeline. BHP is to operate the fields in partnership with Sonatrach. The $900 million In Amenas project is due to come onstream in 2004 and to produce over 700 million cubic feet per day of natural gas. Liquefied Natural Gas (LNG) Exports Electricity Legislation pending in parliament would end the monopoly over power production held by state-run Sonelgaz and clear the way for Algeria's first independent power projects (IPPs). According to the Middle East Economic Digest , IPPs totaling $12 billion are planned. These include: 1) a 1,200 MW-Hadjret Ennous plant near Tipasa, scheduled for completion in 2003-4; 2) a 2X600-MW Terga plant near Oran Tipasa, scheduled for completion in 2005-6; and 3) a 2X600-MW Koudiat Draouch plant near Annaba, scheduled for completion in 2003-4. In the nearer term, the 440-MW Hamma natural gas, combined-cycle turbine plant in Algiers is moving ahead toward commissioning in early 2002. The plant, being built by Sonelgaz, was originally planned as a private project, but is instead being funded with Arab and Islamic financing. Private financing is also planned for a three-by-100-MW gas turbine unit at Hassi Messaoud. Future plans include natural-gas-fired power plants at Arzew, Hadjret En Nouss, Koudiat Draouch, Skikda, Terga and more. In December 2001, Sonelgaz signed a joint venture agreement with Italian power grid manager GRTN on the possibility of constructing an undersea power cable to export electricity to Europe via Italy. In November 2001, Sonelgaz signed a similar deal with Spain's power group Red Electrica de Espana to build an underwater power line between Algeria and Spain. Currently, Algeria has two links to the Moroccan electricity grid and supplies over 550 gigawatthours (GWh) of electricity to Morocco. In May 2001, Sonatrach and Sonelgaz established a joint venture -- the Algerian Energy Company -- to export electricity. Sonatrach has a $107-million contract with Anadarko and Italy's GE Nuovo Pignone to build the country's first privately financed natural-gas-fired power plant at Hassi Berkine. GE Nuovo Pignone, a subsidiary of General Electric, will also provide a gas treatment system, liquid fuel gas turbine storage and services. MAURITANIA Energy The overwhelming majority (99%) of Mauritania's commercial energy consumption in 1999 was oil, all of which was imported. Mauritania also consumes a significant percentage of "non-commercial" (i.e., wood, biomass) energy. MOROCCO Morocco's real gross domestic product is expected to grow by around 2.5%-3% in 2002, down sharply from 7.6% growth in 2001. In 2001, the agricultural sector, which makes up a large share (around 17%-20%) of Morocco's economy and workforce (around 40%-50%), was suffering from the third drought year in a row. Morocco's vulnerability to erratic rainfall patterns, and therefore agricultural output, has encouraged the government in its attempts at economic diversification, particularly towards manufacturing and services (including tourism). Morocco has a strong and growing tourism sector (although this appears to have been set back somewhat in the aftermath of the September 11, 2001 terrorist attack on the United States, with an estimated 100,000 hotel reservations cancelled as of early December 2001), plus an expanding manufacturing base. In 2000, an oil and gas discovery (of unknown magnitude) in the Talsint region near the border with Algeria raised hopes that Morocco could add another important asset to its economy, help cut the country's energy import bill (now around $1-$1.5 billion per year) and also attract new investment to the country. In the meantime, however, lower oil import prices (such as in recent months)generally are helpful to Morocco's economy. Morocco maintains relatively tight fiscal and monetary policies, and this has helped reduce the country's fiscal deficit from 10% of GDP in the 1980s to less than 3% currently. Morocco's inflation rate (consumer prices) is expected to average around 2.5% in 2002, up slightly from 2.0% in 2001. Foreign direct investment (FDI) levels held steady in 2001, at approximately $3 billion. On January 9, 2002, King Mohammed VI announced plans for a series of economic and administrative measures aimed at promoting foreign investment in Morocco. Morocco's current five-year economic plan, which runs from 1999-2004, calls for promoting job creation (unemployment is a serious problem in Morocco), exports and tourism, accelerating the country's privatization process (as of late 2001, the program -- begun in 1993 -- had largely stalled, although a 35% share in Maroc Telecom was sold off to France's Vivendi), upgrading of infrastructure, and reducing social inequalities (especially between urban rich and rural poor. The government also is considering imposing a value-added tax (VAT), as well as direct taxes on business and individual income. Morocco has pursued an economic reform program supported by significant lending from the World Bank and International Monetary Fund (IMF) since the early 1980s. This reform program has, at the IMF's urging, liberalized the foreign exchange regime, lowered tariffs and other trade barriers, reformed the banking system, restrained government spending, reduced the foreign debt burden (in part through "debt-for-equity" swaps, in part through refinancing), and encouraged foreign investment (now permitted in most sectors of the economy). Morocco also has signed several agreements with the European Union on economic cooperation, including one establishing a free trade zone for industrial goods over a 12-year transition period. The European Free Trade Association (EFTA), as it is known, came into effect on December 4, 1999, following ratification by both sides. Morocco traditionally has had almost no energy reserves (although recent oil and gas finds may be about to change this), but does contain the world's largest phosphate reserves, and produces significant amounts of fertilizers and phosphoric acid. Morocco imports around 90% of its energy needs, including significant amounts of oil (about $900 million in 1999) and coal. The government is encouraging increased coal and hydroelectricity production. Coal imports and phosphate exports travel largely through the deepwater port of Jorf Lasfar, which is also the site of a $1-billion phosphoric acid plant and a coal-fired power plant (see below). As of early 2002, the decades-old dispute between Morocco and the Polisario Liberation Front over the Western Sahara continues. A referendum on the future of the territory, a former Spanish colony which has rich phosphate deposits, was scheduled for January 1992 under U.N. auspices, but has yet to be held. In December 1999, the U.N. Security Council voted to keep the U.N. mission in Western Sahara through February 2000. On February 18, 2000, U.N. Secretary General Kofi Annan stated that the core problem of determining who is eligible to vote on the question of independence for the Western Sahara region "could...prevent the holding of the referendum" indefinitely. In January 2001, the Polisario said that it remained in a state of war with Morocco over the Western Sahara. In November 2001, the king made the first visit to the Western Sahara by a Moroccan monarch in 16 years. Oil and

Gas Besides Talsint, other areas of Morocco which are being explored include: 1) the Loukos South Offshore block in the Atlantic Ocean north of Rabat, in which Lone Star holds acreage; 2) the Al Hoceima-Nador Offshore area in the Mediterranean, in which Conoco holds a reconnaissance license; 3) the Cap Draa Haute Mer Offshore area south of Agadir, in which Kerr-McGee, Enterprise Oil, and Energy Africa hold shares; 4) offshore blocks (Safi Haute Mer and Ras Tafeilney) south of Rabat, in which U.S. Vanco Energy Co. and the U.K.'s Lasmo have oil exploration agreements; 5) a block at Labrouj in the center of the country, for which Lone Star has a contract; 6) an area around Ounoura, on the Atlantic coast near Essaouira, and for which Lone Star plans to invest $50 million; 7) five deepwater blocks (Rimella A-E) on the Atlantic coast south of Agadir, for which Shell Maroc has signed an 8-year exploration agreement; 8) the Tiznit offshore area, in which Sweden's Taurus Oil and Energy Africa have exploration permits; and 9) the western Prerif, for which Anschutz and Enterprise Oil have exploration licenses. In late 2000/early 2001, Morocco's state oil company ONAREP (Office National de Recherches et d'Exploitation Petrolieres) opened bidding on Morocco's first offshore licensing round. The bidding -- for exploration permits on eight blocks in the Atlantic Ocean offshore the Rabat-Safi area -- has been extended several times to allow more oil companies to study the seismic data. In October 2001, Morocco signed two controversial oil exploration deals, both offshore the disputed Western Sahara region. The two contracts were with: 1) TotalFinaElf for the Dakhla Offshore zone; and 2) Kerr-McGee for a 44,000-square-mile area off the Western Sahara coast. These deals would mark the first such authorizations by Morocco in the disputed territory, which is believed to be potentially rich in oil reserves. The Polisario Front, which has fought Morocco for years over the Western Sahara region, protested the contracts to the United Nations, which is now examining the issue from a legal perspective. The Polisario also called on the European Union to cancel what it calls the "illegal and illicit" contract between Morocco and TotalFinaElf. Currently, Morocco produces small volumes of natural gas from the Gharb Basin in the north, including the Meskala field just north of Essaouira. In January 2000, an energy ministry spokesman said that Morocco would soon issue new tax exemptions and other incentives to help attract foreign investors to explore for oil in Morocco. In March 2000, Morocco modified its hydrocarbons law in order to, among other things, offer a 10-year tax break to offshore oil production firms and to reduce the government's stake in future oil concessions (to a maximum of 25%). In late December 2001, Morocco stated that an offshore exploration area granted by Spain to Repsol actually was in Moroccan territorial waters. The area, over which Spain's cabinet approved nine, six-year licenses, is located close to Spain's Canary Islands, and about 56 miles northwest of Morocco's coastal Tarfaya region. In October 1998, International Petroleum Investment Company (IPIC) of Abu Dhabi and Spanish Energy Company Cepsa formed a 50-50 joint venture called Cepsa Maghreb to market and distribute petroleum products and LPG in Morocco. Products are to be supplied from Cepsa's refineries in Spain, and French company Vitogaz is building an LPG import terminal and tank farm near Casablanca. Morocco has two refineries (Mohammedia and Sidi Kacem) which have combined capacity of 154,901 bbl/d. Refining company Samir reportedly is planning to invest around $600 million over the next 5 years to modernize its refineries and to expand capacity. Samir has a 125,230-bbl/d refinery at Mohammedia (near Casablanca), which it plans to expand to 160,000 bbl/d (at a cost of $20 million). On September 1, 2000, Morocco decided to increase the price of petroleum products in the country by 4.8%-10.8%, largely in response to increased world oil prices, as well as a weaker currency against the dollar. Morocco contains only small natural gas reserves -- around 100 billion cubic feet (bcf), with about 85% located in the Essaouira Basin, and the rest in the Rharb and Pre-Rif basins. This does not count any possible additional reserves at Talsint. Besides its own domestic gas reserves, Morocco is a major transit center for Algerian gas exports across the Strait of Gibraltar to Spain, via the 300-bcf/year, Maghreb-Europe Gas (MEG) pipeline (also known as the Pedro Duran Farell pipeline). In November 1999, Spanish company Natural Gaz SDG announced its intention to invest up to $400 million in a natural gas distribution network for Morocco. Coal and

Electricity

With electricity demand increasing at around 7% annually, Morocco is planning several new power plants, and also a power sector liberalization aimed at opening 20% of the sector to competition by 2003 (with more later). Morocco recently completed a major expansion of its $1.5-billion, coal-fired Jorf Lasfar plant (Africa's largest independent power plant) with the addition of two, 348-megawatt (MW), units by U.S.-based CMS Energy Corp. In early February 2001, CMS announced that Unit 4 had been completed, raising Jorf Lasfar's total power generating capacity to 1,356 MW, enough to supply more than half of Morocco's total power requirements. Units 1, 2, and 3 of Jorf Lasfar were completed in 1994, 1995, and June 2000, respectively. The plant is located on the Atlantic coast about 80 miles southwest of Casablanca. Currently, Morocco has 25 hydroelectric power plants, 5 steam thermal facilities, nine turbine stations, and numerous diesel plants. Morocco's National Office of Electricity (ONE) has an ambitious plan to supply the countryside with electricity by 2010 (currently, only around 15% of the rural population has access to electricity). Morocco plans to spend around $3.7 billion on energy projects through 2003, and part of this money will go towards building power plants and towards rural electrification. As part of this plan, a new, $500-million, 350-400-MW combined-cycle power plant, to be fired by natural gas from the MEG pipeline, is planned. The plant, Morocco's third independent power project (IPP), is to be built at Tahaddart, near Tangier in northern Morocco. In November 2001, Spain's Endesa signed an agreement to build and operate the 334-MW plant. Other future power plants are planned for Aon Beni Mathar (180 MW), Dhar Sadane (75 MW), Sendouk (65 MW), and Tarfaya (60 MW). In October 2000, the United States and Morocco signed an agreement on cooperation in energy efficiency and renewable energy. In September 2000, Spain and Morocco, which put in place a 350-MW interconnection in 1998, agreed to study the potential for further linkage of the two countries' electricity grids. In December 2001, Endesa became the first Spanish company to import electricity from Morocco. ONE also is looking at to increase renewable energy's share of Morocco's total power consumption considerably in coming years. ONE is looking at solar power, as well as at building wind power parks throughout the country (including farms at Tangier and Tarfaya). In late 1998, ONE awarded a $56-million construction contract to a French joint venture (CED) for a 50-MW wind farm to be built at Koudia el Beida near the Straight of Gibraltar. In April 2000, Morocco said that it would build a 10-MW wind power plant in the northern city of Tetouan. If completed, this would be the first wind farm in Africa and the Arab world, according to ONE. Meanwhile, a potential project to build a 50-MW solar power plant at Ouarzazate has been postponed, while a 180-MW thermo-solar plant at Ain Beni Mathar is in the planning stages. Morocco also has expressed interest in nuclear power for desalination and other purposes, and in September 2001 signed an agreement with the United States establishing the legal basis for construction of a 2-MW research reactor just east of Rabat. TUNISIA The Tunisian government, headed by President Zine al-Abedine Ben Ali (now in the midst of his third, five-year term, which runs through October 2004) and his Constitutional Democratic Rally (RCD) party, appears determined to continue liberalizing and reforming the country's economy, although at a pace which does not provoke popular unrest. In September 2001, President Ben Ali was nominated to stand as a candidate in the next presidential election, despite a constitutional ruling which bars Ben Ali from a fourth term. In December 2001, the parliament approved the country's 2002 budget, which aims to reduce the deficit to 2.2% of GDP (from 2.4% in 2001). The IMF is pushing Tunisia to accelerate its reform efforts (i.e., reducing the fiscal deficit by cutting spending), but the government is concerned not to move too rapidly. In December 2001, the IMF issued a generally positive report on Tunisia's economy, stressing the importance of continued privatization, cuts in subsidies, restructuring of the country's banking and financial sector, and multilateral trade liberalization. In regard to the last IMF objective (trade liberalization), a 1995 European Union (EU)-Tunisia association agreement went into effect in 1998, under which Tunisia is to dismantle its customs barriers to European goods over a 12-year period. On January 1, 2000, tariff barriers were lifted for European manufactured goods on "List 4" (consumer goods which have an equivalent in Tunisia), exposing Tunisian consumer goods to EU competition. Around 75%-80% of Tunisia's exports go to the EU. To replace lost customs revenues, Tunisia is attempting to improve its collection of taxes domestically. In May 2001, Egypt, Jordan, Morocco and Tunisia agreed to set up a free trade zone ahead of the 2010 target for trade barriers to end in the Euro-Mediterranean area. Oil

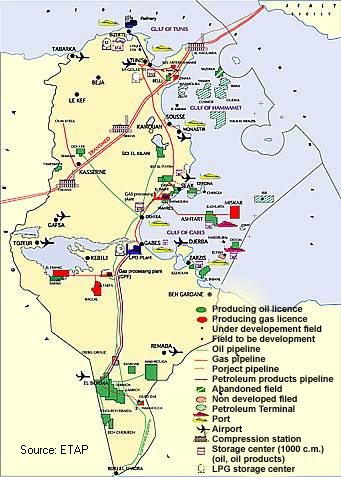

Tunisia's state-owned oil company is Enterprises Tunisienne d'Activites Petrolieres (ETAP). ETAP is seeking to encourage exploration, especially in the northern part of the country, the northern coast, and the Gulf of Hammamet. It believes the development of new, smaller fields in cooperation with independent companies is the way to accomplish this. ETAP expects foreign oil companies to spend $120 million on exploration in Tunisia this year, versus just $86 million in 2000. Tunisia reformed its hydrocarbons laws in August 2000, in hopes of attracting just such upstream investment. One of the most important provisions is a reduction in the tax rate from 75% to 50% for foreign firms if ETAP takes a 40% share of the concession. Royalties are are fixed at 10% for oil and 8% for gas. Foreign companies currently operating in Tunisia include Agip, Anadarko, Anschutz, Lasmo, Marathon, and Petro-Canada. In addition to obtaining self-sufficiency in production for Tunisia, ETAP is pursuing overseas exploration and production. The company is working in Syria with Preussag of Germany to develop small oilfields and is studying possibilities in Yemen and Iraq. In January 2001, Tunisian Industry Minister Moncef Ben Abdallah met with undersecretary of the Iraqi Oil Ministry Fay'iz Abdallah Shahin to discuss cooperation in petroleum development. ETAP has a joint venture with Sonatrach of Algeria to explore a border area and also with Libya's National Oil Company exploring an offshore block. Tunisia's largest oilfield is El Borma, discovered in 1964 near the Algerian border. Its production is 19,920 bbl/d. Ashtart (production 16,840 bbl/d) is the only other oilfield with proven and estimated reserves over 100 million barrels. About 75% of Tunisian oil production comes from these two fields and the Sidi El Kilani field (13,260 bbl/d). The Al Manzah field started production at 4,000 bbl/d in October 2000. Centurion of Canada is the operator. In July 2001, Dallas-based Pioneer Natural Resources Company announced that subject to Tunisian government approval its subsidiary, Pioneer Natural Resources Anaguid Ltd., has entered into definitive agreements with Coho Anaguid, Inc., a subsidiary of Coho Energy, Inc., Anadarko Tunisia Anaguid Company, an indirect wholly-owned subsidiary of Anadarko Petroleum Corporation, and Nuevo Energy Company to jointly acquire Coho's 45.83% participating interest in the Anaguid permit in the Ghadames basin onshore southern Tunisia. Pioneer will join Anadarko, the operator of the permit, and Nuevo in exploring the 1.1-million-acre permit. Earlier, in May 2001, Pioneer began building a position in Tunisia when it acquired a 50% stake in three permits covering 2.7 million acres in the Ghadames basin from Eurogas of Calgary in return for drilling two wells in the area at a cost of $5.2 million. An important discovery of the past year was the Oued Zaar (Tataouine) field, with estimated reserves of 15 million barrels. In September 2001, ETAP opened tenders for 20 blocks, including onshore blocks C1-C4 (central Tunisia) and S1-S5 (south Tunisia), plus offshore blocks N1-N4 (northern Tunisia) and E1-E7 (eastern Tunisia). A 22,000-bbl/d, 78-mile pipeline between the Sidi El Kilani oilfield and the port of Skhirra was inaugurated in March, 2001. Natural

Gas Baker Hughes reportedly is farming out 75% interests in its oil and gas concessions in northern Tunisia and northern Egypt. This includes the offshore Zembra block, which incorporates most of the Gulf of Tunis, and in which it holds a 100% interest (after Maxus Energy relinquished its share in June 1998). A natural gas pipeline also is set to link Libya and Tunisia by 2003, with Libyan natural gas supplies being sold to Tunisia. The Transmediterranean pipeline that transports 25 Bcf Algerian natural gas to Italy per year runs through Tunisia. Tunisia receives some royalties from this pipeline as payment for access through its territory. Electricity In late 1999, financing on the $250-million Rades, 471-megawatt (MW), gas-fired power project was completed. A consortium comprised of U.S.-based PSEG (60%), and Japan's Marubeni (40%) is developing the project on a 20-year build-own-operate-transfer (BOOT) basis. Rades -- Tunisia's first independent power plant -- is expected to become operational in 2002. Natural gas for the Rades plant is to be supplied from various Tunisian sources. Tunisia's state-owned gas and power company, STEG (Societe Tunisienne de l'Electricite et du Gaz) has signed a 20-year power-purchase agreement with the consortium building Rades. BG is planning to build a $200-million, 500-MW power plant near Sfax that will use gas from the Miskar, and eventually, Hasdrubal fields. BG will likely partner with STEG or ETAP, and the facility should be operational in 2006. Besides Rades, a Build-Own-Operate plant, El Biban, is being built as well. Construction on El Biban began in July 2001. Libya and Tunisia are working on linking their electricity grids after a meeting of Arab energy ministers in April 2001, emphasized the importance of completing the project of linking all Arab countries' electricity grids. Red Electrica of Spain and Transenergie of Canada have been awarded a contract to advise the two governments on implementing the connection.

Sources: Economist Intelligence Unit; Central Intelligence

Agency World Factbook 2001. PPP=Purchasing Power Parity.

Source:

Energy Information Administration

Source:

Energy Information Administration

Sources

for this report include: Africa Research Bulletin, AP Worldstream,

Business Wire, CIA World Factbook 2001, Economist Intelligence Unit,

Energy Day, Financial Times, Middle East Economic Digest, Middle East

Executive Reports, Oil and Gas Journal, Petroleum Economist, Petroleum

Intelligence Weekly, PR Newswire, U.S. Energy Information Administration,

World Gas Intelligence, World Markets Online.

For more

information from EIA on Algeria, Mauritania, Morocco, and Tunisia, please

see: Links to other U.S. government sites: The Center for Middle Eastern

Studies - Algeria If you

liked this Country Analysis Brief or any of our many other Country

Analysis Briefs, you can be automatically notified via e-mail of updates.

Simply click here, select "international" and

the specific list(s) you would like to join, and follow the instructions.

You will then be notified within an hour of any updates to our Country

Analysis Briefs.

File last modified: January 14, 2002 Contact:

URL: http://www.eia.doe.gov/cabs/maghreb.html If you are having technical problems with this site, please contact the EIA Webmaster at wmaster@eia.doe.gov |

Real GDP growth in

Mauritania is expected to be a strong 5.0% in 2002, following estimated

growth of 4.6% in 2001 and 4.4% in 2000. Inflation is forecast at only

2.5%, down slightly from 3.0% in 2001, and the country appears to moving

forward with a privatization and economic reform program. Despite these

positive signs, Mauritania remains a poor country (more than half the

population lives on less than $1 per day) with a rapidly growing

population and many social and economic problems. Mauritania also remains

heavily reliant on foreign aid and debt relief (in March 2000, the Paris

Club eased Mauritania's debt service burden as a reward for the country's

moves towards economic reform). In early November 2001, President Maaouya

Ould Sid'Ahmed Taya (who came to power in 1984) refused to accept the

resignation of Prime Minister Cheikh el Avia Ould Mohamed Khouna (first

appointed in November 1998), following a relatively strong showing by

opposition parties in October voting (the ruling Democratic and Socialist

Republican Party won the election). In early January 2002, the government

banned the "Action for Change" opposition party.

Real GDP growth in

Mauritania is expected to be a strong 5.0% in 2002, following estimated

growth of 4.6% in 2001 and 4.4% in 2000. Inflation is forecast at only

2.5%, down slightly from 3.0% in 2001, and the country appears to moving

forward with a privatization and economic reform program. Despite these

positive signs, Mauritania remains a poor country (more than half the

population lives on less than $1 per day) with a rapidly growing

population and many social and economic problems. Mauritania also remains

heavily reliant on foreign aid and debt relief (in March 2000, the Paris

Club eased Mauritania's debt service burden as a reward for the country's

moves towards economic reform). In early November 2001, President Maaouya

Ould Sid'Ahmed Taya (who came to power in 1984) refused to accept the

resignation of Prime Minister Cheikh el Avia Ould Mohamed Khouna (first

appointed in November 1998), following a relatively strong showing by

opposition parties in October voting (the ruling Democratic and Socialist

Republican Party won the election). In early January 2002, the government

banned the "Action for Change" opposition party.  King Hassan

II, ruler of Morocco since 1961, died on July 23, 1999, and was succeeded

by his son, Mohammed VI. The new King is believed to be an advocate of

economic reform and political liberalization, but to date the record has

been mixed at best. In June 2000, King Mohammed VI paid his first visit to

the United States and met with President Clinton.

King Hassan

II, ruler of Morocco since 1961, died on July 23, 1999, and was succeeded

by his son, Mohammed VI. The new King is believed to be an advocate of

economic reform and political liberalization, but to date the record has

been mixed at best. In June 2000, King Mohammed VI paid his first visit to

the United States and met with President Clinton. Tunisia's real

gross domestic product (GDP) is expected to grow by a solid 4.0% in 2002,

the same as in 2001, but down from 4.7% growth in 2000 and 6.1% growth in

1999. Inflation is expected to remain low in 2002, following estimated

inflation of around 3% in 2001. Foreign direct investment (FDI) has

increased in Tunisia from 488 million Tunisian dinars in 1999 to 1.1

billion Tunisian dinars in 2000, of which 320 million dinars was in the

energy sector. Some of the FDI has come from privatizations. In late 2000

the government announced that an additional 41 companies would begin to be

privatized in 2001, with proceeds expected to be over $1.2 billion.

Despite all this, unemployment remains at high levels (officially 16%, but

unofficially much higher), there are signs of growing social pressures,

and the country's debt burden is expected to increase in 2002. Estimates

for the country's crucial tourist industry (Tunisia's main source of

foreign currency earnings and second largest employer) in the aftermath of

the September 11, 2001 terrorist attacks on the United States already have

been lowered for 2001, and this downturn could continue during

2002.

Tunisia's real

gross domestic product (GDP) is expected to grow by a solid 4.0% in 2002,

the same as in 2001, but down from 4.7% growth in 2000 and 6.1% growth in

1999. Inflation is expected to remain low in 2002, following estimated

inflation of around 3% in 2001. Foreign direct investment (FDI) has

increased in Tunisia from 488 million Tunisian dinars in 1999 to 1.1

billion Tunisian dinars in 2000, of which 320 million dinars was in the

energy sector. Some of the FDI has come from privatizations. In late 2000

the government announced that an additional 41 companies would begin to be

privatized in 2001, with proceeds expected to be over $1.2 billion.

Despite all this, unemployment remains at high levels (officially 16%, but

unofficially much higher), there are signs of growing social pressures,

and the country's debt burden is expected to increase in 2002. Estimates

for the country's crucial tourist industry (Tunisia's main source of

foreign currency earnings and second largest employer) in the aftermath of

the September 11, 2001 terrorist attacks on the United States already have

been lowered for 2001, and this downturn could continue during

2002.