January 2003

Mauritania | Morocco | Tunisia | Links

Arab Maghreb Union

The Arab Maghreb Union (AMU), which includes Mauritania, Morocco,

and Tunisia (note: due to their size and importance, Algeria and Libya are covered

in separate reports, is an important oil and gas producer, exporter, and

transit center to southern Europe. Natural gas production from the region

is increasing rapidly, and new pipelines to Spain and Italy are being

planned.

Note: Information contained in this report is the best available as of January 2003 and is subject to change.

MAURITANIA Real GDP growth in Mauritania is expected to be a

strong 5.0% in 2003, following estimated growth of 5.0% in 2002. Inflation

is forecast at only 3.0%, up slightly from 2.5% in 2002, and the country

appears to moving forward with a privatization and economic reform

program. In March 2002, for instance, four companies (ONE of Morocco,

Union Fenosa, Vivendi, and Anglo-American) submitted bids on the country's

state power company.

Real GDP growth in Mauritania is expected to be a

strong 5.0% in 2003, following estimated growth of 5.0% in 2002. Inflation

is forecast at only 3.0%, up slightly from 2.5% in 2002, and the country

appears to moving forward with a privatization and economic reform

program. In March 2002, for instance, four companies (ONE of Morocco,

Union Fenosa, Vivendi, and Anglo-American) submitted bids on the country's

state power company.

Despite these positive signs, Mauritania remains a poor country (more than half the population lives on less than $1 per day) with a rapidly growing population and many social and economic problems. Mauritania also remains heavily reliant on foreign aid and debt relief (in March 2000, the Paris Club eased Mauritania's debt service burden as a reward for the country's moves towards economic reform). In January 2002, Mauritania was hit by torrential rains which caused significant damage to crops, livestock, and grazing land in southern regions of the country.

President Maaouya Ould Sid'Ahmed Taya (who came to power in 1984) continues to push ahead with economic reforms efforts. As a consequence, Mauritania has attracted significant amounts of donor funds and also managed (in Juner 2002) to reach the completion point under the World Bank/International Monetary Fund (IMF) heavily indebted poor countries (HIPC) initiative. This qualifies Mauritania for full debt relief, and should reduce its external debt-service payments by around 50%. In general, Mauritania has achieved a solid economic performance record according to the IMF.

The World Trade Organization's (WTO's) evaluation of Mauritania points to several challenges for the country's economic progress. These include: supply-side constraints (i.e., a limited number of exportable products); infrastructure problems; and limited human resources. The WTO points to the country's mining sector as offering great potential, while pointing out that the manufacturing and tourism sectors are underdeveloped. Currently, mining and fishing account for the vast majority of Mauritania's exports. Foreign aid also continues to be very important. In April 2002, the EU and Mauritania signed a strategic cooperation agreement setting forth guidelines for disbursement of $144 million in European Development Funds over the next five years.

Energy

Mauritania has not traditionally

been thought of as a promising hydrocarbons area, but this may now be

changing as exploration has yielded some positive signs. In May 2001, for

instance, a consortium of energy companies led by Australia's Woodside

Petroleum made a significant oil discovery with its Chinguetti-1 well,

located in deep waters off the country's southwest coast, and in October

2002, the Chinguetti 4-4 appraisal well confirmed the presence of

oil-bearing geological structures. In addition, the Banda prospect in

Chinguetti is believed to contain as much as 100 million barrels of oil

plus several trillion cubic feet of natural gas. In general, it is

believed that Mauritania may contain significant oil deposits off its

coast. Foreign oil companies operating in Mauritania include: British

Borneo, Dana Petroleum, Elixir, Fusion, Hardman, and Woodside Petroleum.

The overwhelming majority (99%) of Mauritania's commercial energy consumption in 1999 was oil, all of which was imported. Mauritania also consumes a significant percentage of "non-commercial" (i.e., wood, biomass) energy.

MOROCCO  King Hassan II, ruler of Morocco since 1961, died on July 23,

1999, and was succeeded by his son, Mohammed VI. The King is believed to

be an advocate of economic reform and political liberalization, but,

generally speaking, economic reform has proceeded slowly in recent years.

One example is liberalization of the country's domestic oil market,

promised in 1997 but not yet carried out. State-owned sugar and tobacco

companies reportedly are slated for sale in 2003.

King Hassan II, ruler of Morocco since 1961, died on July 23,

1999, and was succeeded by his son, Mohammed VI. The King is believed to

be an advocate of economic reform and political liberalization, but,

generally speaking, economic reform has proceeded slowly in recent years.

One example is liberalization of the country's domestic oil market,

promised in 1997 but not yet carried out. State-owned sugar and tobacco

companies reportedly are slated for sale in 2003.

Morocco's real gross domestic product is expected to grow by around 4% in 2003, up from 2.2% growth in 2002 but down sharply from the 7.6% growth achieved in 2001. In November 2002, Morocco was afflicted by heavy rains and severe flooding which caused major infrastructure damage near Casablanca. This flooding has now occurred two years in a row, following three years of drought, during which the country's large agricultural sector (accounting for around a fifth of GDP and more than two-fifths of the workforce) was adversely affected. Morocco's vulnerability to erratic rainfall patterns, and therefore agricultural output, has encouraged the government in its attempts at economic diversification, particularly towards manufacturing and services (including tourism). Prime Minister Driss Jettou's government has initiated a $100 million emergency program to repair damaged infrastructure and protect vulnerable areas from future floods.

Prior to the terrorist attacks of September 11, 2001, Morocco had a strong and growing tourism sector, although this appears to have been set back somewhat in the aftermath of that event. Tourism also is being hurt by the general perception of Middle East political instability. On the positive side, Morocco's hard currency reserves were up as of July 2002, while the trade balance also has improved as exports have risen.

In 2000, an oil and gas discovery (of unknown magnitude) in the Talsint region near the border with Algeria raised hopes that Morocco could add another important asset to its economy, help cut the country's energy import bill (now around $1-$1.5 billion per year) and also attract new investment to the country. Morocco also has an expanding manufacturing base.

Morocco maintains relatively tight fiscal and monetary policies, with the 2003 budget calling for only a small increase in spending, and this has helped sharply reduce the country's fiscal deficit. Morocco's inflation rate (consumer prices) is expected to average around 3.0% in 2003, up slightly from 2.5% in 2002. On January 9, 2002, King Mohammed VI announced plans for a series of economic and administrative measures aimed at promoting foreign investment in Morocco.

Morocco's current five-year economic plan, which runs from 1999 through 2004, calls for promoting job creation (unemployment is a serious problem in Morocco, at 13% or higher), exports and tourism, accelerating the country's privatization process (as of late 2001, the program -- begun in 1993 -- had largely stalled, although a 35% share in Maroc Telecom was sold off to France's Vivendi), upgrading of infrastructure, and reducing social inequalities (especially between urban rich and rural poor. The government also has considered imposing a value-added tax (VAT), as well as direct taxes on business and individual income.

Morocco has pursued an economic reform program supported by significant lending from the World Bank and International Monetary Fund (IMF) since the early 1980s. This reform program has, at the IMF's urging, liberalized the foreign exchange regime, lowered tariffs and other trade barriers, reformed the banking system, restrained government spending, reduced the foreign debt burden (in part through "debt-for-equity" swaps, in part through refinancing), and encouraged foreign investment (now permitted in most sectors of the economy). Morocco also has signed several agreements with the European Union on economic cooperation, including one establishing a free trade zone for industrial goods over a 12-year transition period. The European Free Trade Association (EFTA), as it is known, came into effect on December 4, 1999, following ratification by both sides.

Morocco traditionally has had almost no energy reserves, but does contain the world's largest phosphate reserves, and produces significant amounts of fertilizers and phosphoric acid. Morocco imports around 90% of its energy needs, including significant amounts of oil (about $900 million in 1999) and coal. The government is encouraging increased coal and hydroelectricity production. Coal imports and phosphate exports travel largely through the deepwater port of Jorf Lasfar, which is also the site of a $1-billion phosphoric acid plant and a coal-fired power plant (see below).

As of early 2003, the decades-old dispute between Morocco and the Polisario Liberation Front over the Western Sahara continues. A referendum on the future of the territory, a former Spanish colony which has rich phosphate deposits, was scheduled for January 1992 under U.N. auspices, but has yet to be held. In December 1999, the U.N. Security Council voted to keep the U.N. mission in Western Sahara through February 2000. On February 18, 2000, U.N. Secretary General Kofi Annan stated that the core problem of determining who is eligible to vote on the question of independence for the Western Sahara region "could...prevent the holding of the referendum" indefinitely. In January 2001, the Polisario said that it remained in a state of war with Morocco over the Western Sahara. In November 2001, the king made the first visit to the Western Sahara by a Moroccan monarch in 16 years.

Oil and Natural Gas

Morocco contains

insignificant proven oil reserves of 1.6 million barrels, although most

sedimentary basins (especially offshore on the Atlantic continental shelf

or in deep waters off the shelf) in the country have not been explored,

and Morocco is actively pursuing expansion of its upstream oil and natural

gas sector. At present, the country relies on imports for nearly all of

its oil consumption needs (around 150,000 bbl/d), except for about 200

barrels per day (bbl/d) from its Sidi Rhalem field, located in the

Essaouira Basin. This could change in coming years with a possibly

significant discovery in August 2000 by Lone Star, a local subsidiary of

US-based Skidmore, of oil at Talsint, near the border with Algeria.

Initial reports indicated that Talsint contained as much as 20 billion

barrels equivalent of oil and natural gas. This was soon lowered to 1-2

billion barrels, then to 100 million barrels. Many oil analysts are

skeptical that Talsint contains even this much recoverable oil and gas,

and so far, Lone Star's well (Sidi Belkacem #1) at Talsint only has proven

reserves of 10 million barrels or less of total hydrocarbons (the exact

mix of oil and natural gas is unknown).

Besides Talsint, other areas of Morocco which are being explored include: 1) the Loukos South Offshore block in the Atlantic Ocean north of Rabat, in which Lone Star holds acreage; 2) the Al Hoceima-Nador Offshore area in the Mediterranean, in which Conoco holds a reconnaissance license; 3) the Cap Draa Haute Mer Offshore area south of Agadir, in which Kerr-McGee, Enterprise Oil, and Energy Africa hold shares; 4) offshore blocks (Safi Haute Mer and Ras Tafeilney) south of Rabat, in which U.S. Vanco Energy Co. and the U.K.'s Lasmo have oil exploration agreements; 5) a block at Labrouj in the center of the country, for which Lone Star has a contract; 6) an area around Ounoura, on the Atlantic coast near Essaouira, and for which Lone Star plans to invest $50 million; 7) five deepwater blocks (Rimella A-E) on the Atlantic coast south of Agadir, for which Shell Maroc has signed an 8-year exploration agreement; 8) the Tiznit offshore area, in which Sweden's Taurus Oil and Energy Africa have exploration permits; and 9) the western Prerif, for which Anschutz and Enterprise Oil have exploration licenses. In late 2000/early 2001, Morocco's state oil company ONAREP (Office National de Recherches et d'Exploitation Petrolieres) opened bidding on Morocco's first offshore licensing round. The bidding -- for exploration permits on eight blocks in the Atlantic Ocean offshore the Rabat-Safi area -- has been extended several times to allow more oil companies to study the seismic data.

In October 2001, Morocco signed two controversial oil exploration deals, both offshore the disputed Western Sahara region. The two contracts were with: 1) TotalFinaElf for the Dakhla Offshore zone; and 2) Kerr-McGee for a 44,000-square-mile area off the Western Sahara coast. These deals would mark the first such authorizations by Morocco in the disputed territory, which is believed to be potentially rich in oil reserves. The Polisario Front, which has fought Morocco for years over the Western Sahara region, protested the contracts to the United Nations, which stated that the contracts were not illegal in and of themselves, as long as the resources were developed for the benefit of the people living in the region. The Polisario also called on the European Union to cancel what it calls the "illegal and illicit" contract between Morocco and TotalFinaElf.

Currently, Morocco produces small volumes of natural gas from the Gharb Basin in the north, including the Meskala field just north of Essaouira. In January 2000, an energy ministry spokesman said that Morocco would soon issue new tax exemptions and other incentives to help attract foreign investors to explore for oil in Morocco. In March 2000, Morocco modified its hydrocarbons law in order to, among other things, offer a 10-year tax break to offshore oil production firms and to reduce the government's stake in future oil concessions (to a maximum of 25%).

In February and May 2002, Morocco protested that an offshore exploration area granted by Spain to Repsol actually was in Moroccan territorial waters. The area, over which Spain's cabinet approved nine, six-year licenses, is located close to Spain's Canary Islands, and about 56 miles northwest of Morocco's coastal Tarfaya region.

In October 1998, International Petroleum Investment Company (IPIC) of Abu Dhabi and Spanish Energy Company Cepsa formed a 50-50 joint venture called Cepsa Maghreb to market and distribute petroleum products and LPG in Morocco. Products are to be supplied from Cepsa's refineries in Spain, and French company Vitogaz is building an LPG import terminal and tank farm near Casablanca.

Morocco has two refineries (Samir Oil Refinery at Mohammedia and Sidi Kacem) which have combined capacity of 154,901 bbl/d. In late November, severe flooding led to a massive fire at the Samir Refinery, which produces around 80%-90% of the country's refined petroleum products. In early December 2002, Samir officials said that full repairs could cost $150 million and take 9-13 months, although restoration to 60% capacity reportedly occurred very quickly.

Refining company Samir reportedly is planning to invest around $600 million over the next 5 years to modernize its refineries and to expand capacity. Samir has a 125,230-bbl/d refinery at Mohammedia (near Casablanca), which it plans to expand to 160,000 bbl/d (at a cost of $20 million). On September 1, 2000, Morocco decided to increase the price of petroleum products in the country by 4.8%-10.8%, largely in response to increased world oil prices, as well as a weaker currency against the dollar.

Morocco contains only small natural gas reserves -- around 100 billion cubic feet (bcf), with about 85% located in the Essaouira Basin, and the rest in the Rharb and Pre-Rif basins. This does not count any possible additional reserves at Talsint. Besides its own domestic gas reserves, Morocco is a major transit center for Algerian gas exports across the Strait of Gibraltar to Spain, via the 300-bcf/year, Maghreb-Europe Gas (MEG) pipeline (also known as the Pedro Duran Farell pipeline). In November 1999, Spanish company Natural Gaz SDG announced its intention to invest up to $400 million in a natural gas distribution network for Morocco.

Coal and Electricity

Morocco produces coal from

its one mine at Jerada, and imports coal from the United States, Colombia,

and South Africa. Coal, most of which is imported from South Africa, is

consumed largely by power plants at Mohammedia and Jorf Lasfar.

With electricity demand increasing at around 7% annually, Morocco is planning several new power plants. Currently, Morocco has installed power generating capacity of around 4,000 MW, slated to expand to 5,700 MW by 2004. Morocco recently completed a major expansion of its $1.5-billion, coal-fired Jorf Lasfar plant (Africa's largest independent power plant) with the addition of two, 348-megawatt (MW), units by U.S.-based CMS Energy Corp. In early February 2001, CMS announced that Unit 4 had been completed, raising Jorf Lasfar's total power generating capacity to 1,356 MW, enough to supply more than half of Morocco's total power requirements. Units 1, 2, and 3 of Jorf Lasfar were completed in 1994, 1995, and June 2000, respectively. The plant is located on the Atlantic coast about 80 miles southwest of Casablanca. Currently, Morocco has 25 hydroelectric power plants, 5 steam thermal facilities, nine turbine stations, and numerous diesel plants.

Morocco's National Office of Electricity (ONE) has an ambitious plan to supply the countryside with electricity by 2010 (currently, only around 15% of the rural population has access to electricity). Morocco plans to spend around $3.7 billion on energy projects through 2003, and part of this money will go towards building power plants and towards rural electrification. As part of this plan, a new, $500-million, 350-400-MW combined-cycle power plant, to be fired by natural gas from the MEG pipeline, is planned. The plant, Morocco's third independent power project (IPP), is to be built at Tahaddart, near Tangier in northern Morocco. In November 2001, Spain's Endesa signed an agreement to build and operate the 334-MW plant. Other future power plants are planned for Aon Beni Mathar (180 MW), Dhar Sadane (75 MW), Sendouk (65 MW), and Tarfaya (60 MW). In October 2000, the United States and Morocco signed an agreement on cooperation in energy efficiency and renewable energy.

In September 2000, Spain and Morocco, which put in place a 350-MW interconnection in 1998, agreed to study the potential for further linkage of the two countries' electricity grids. In December 2001, Endesa became the first Spanish company to import electricity from Morocco, while a deal was signed with Spain's Union Fenosa as well. Morocco reportedly supplies as much as 25% of Spain's power consumption needs.

ONE also is looking at to increase renewable energy's share of Morocco's total power production considerably in coming years. In June 2002, Morocco and the United States signed a convention on development of "clean" energy sources. ONE is looking at hydroelectric pumped storage (i.e., the 230-MW Afourir project in the Azilal region south of Rabat), solar power (widely used in many remote, rural areas of the country), as well as at building wind power parks throughout the country (including a 140-MW windfarm at Tangier, a 50-MW farm near Tetouan, and a 60-MW facility at Tarfaya). In May 2002, a consortium led by Total Energie won a contract to supply 16,000 rural homes with solar power. Morocco's Energy and Mines Minister, Mustapha Mansouri, said that this project will "reduce the pressure on woodlands, whose over-exploitation currently threatens the environmental balance." The project also should help Morocco achieve its goal of electrifying 80% of the country's villages (up from around 50% now) by 2008. Morocco also has expressed interest in nuclear power for desalination and other purposes, and in September 2001 signed an agreement with the United States establishing the legal basis for construction of a 2-MW research reactor just east of Rabat.

TUNISIA  Tunisia's real

gross domestic product (GDP) is expected to grow by a solid 4.3% in 2003,

up from 2% growth in 2002. Inflation is expected to remain low in 2003,

most likely below 2%. Privatization is moving ahead slowly, despite

President Ben Ali's call in 2001 for an acceleration in the process. The

country's tourism sector has suffered since the September 2001 terrorist

attacks in the United States, as well as the April 2002 bombing of an

ancient synagogue at El Ghriba on the island of Djerba. Meanwhile,

agriculture has been adversely affected by drought, and Tunisian exports

have been hit by slow economic growth in Europe. Tunisia's unemployment

rate remains at high levels (officially 15%, but unofficially much

higher).

Tunisia's real

gross domestic product (GDP) is expected to grow by a solid 4.3% in 2003,

up from 2% growth in 2002. Inflation is expected to remain low in 2003,

most likely below 2%. Privatization is moving ahead slowly, despite

President Ben Ali's call in 2001 for an acceleration in the process. The

country's tourism sector has suffered since the September 2001 terrorist

attacks in the United States, as well as the April 2002 bombing of an

ancient synagogue at El Ghriba on the island of Djerba. Meanwhile,

agriculture has been adversely affected by drought, and Tunisian exports

have been hit by slow economic growth in Europe. Tunisia's unemployment

rate remains at high levels (officially 15%, but unofficially much

higher).

The Tunisian government, headed by President Zine al-Abedine Ben Ali (now in the midst of his third, five-year term, which runs through October 2004) and his Constitutional Democratic Rally (RCD) party, appears determined to continue liberalizing and reforming the country's economy, although at a pace which does not provoke popular unrest. In April 2002, Tunisia's parliament passed a new constitution that will allow Ben Ali to stand for a fourth, 5-year term in 2004.

The IMF is pushing Tunisia to accelerate its structural reform efforts (i.e., reducing the fiscal deficit by cutting spending), increase privatization, liberalize trade, and diversify its economy. The government, however, is concerned about moving too quickly and stirring up social pressures. For 2002-2006, the government is looking to increase domestic and foreign investment, with a target of $34 billion for the period. The IMF's June 2002 report on Tunisia generally praised the country's "well-coordinated macroeconomic, structural and social policies while urging further reforms and aiming for economic growth of 6% annually over the next five years.

A 1995 European Union (EU)-Tunisia Association Agreement went into effect in 1998, under which Tunisia is to dismantle its customs barriers to European goods over a 12-year period. On January 1, 2000, tariff barriers were lifted for European manufactured goods on "List 4" (consumer goods which have an equivalent in Tunisia), exposing Tunisian consumer goods to EU competition. Around 75%-80% of Tunisia's exports go to the EU. To replace lost customs revenues, Tunisia is attempting to improve its collection of taxes domestically. In May 2001, Egypt, Jordan, Morocco and Tunisia agreed to set up a free trade zone ahead of the 2010 target for trade barriers to end in the Euro-Mediterranean area.

Oil

During the first 10 months of 2002, Tunisia

produced around 78,000 barrels per day (bbl/d) of oil, nearly all of which

was crude oil (3,000 bbl/d was natural gas liquids). This represents a 32%

decline from the country's peak oil output, of 114,000 bbl/d, in 1992.

Meanwhile, domestic petroleum demand is increasing rapidly, and Tunisia

became a net oil importer in 2000 for the first time in over 20 years.

Because Tunisia's refining capacity is low, the country exports crude oil

and imports refined products. Currently, Tunisia has over 300 million

barrels in proven oil reserves, and few new discoveries have been made in

recent years.

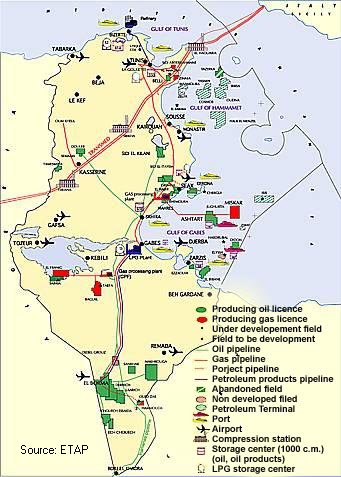

Tunisia's state-owned oil company is Enterprises Tunisienne d'Activites Petrolieres (ETAP). ETAP is seeking to encourage exploration, especially in the northern part of the country, the northern coast, and the Gulf of Hammamet. It believes the development of new, smaller fields in cooperation with independent companies is the way to accomplish this. Tunisia reformed its hydrocarbons laws in August 2000, in hopes of attracting just such upstream investment. One of the most important provisions is a reduction in the tax rate from 75% to 50% for foreign firms if ETAP takes a 40% share of the concession. Royalties are fixed at 10% for oil and 8% for gas.

In addition to obtaining self-sufficiency in production for Tunisia, ETAP is pursuing overseas exploration and production. The company is working in Syria with Preussag of Germany to develop small oilfields and has signed an oil cooperation agreement with Iraq. ETAP has a joint venture with Sonatrach of Algeria to explore a border area and also with Libya's National Oil Company exploring an offshore block.

Tunisia's largest oilfield is El Borma, discovered in 1964 near the Algerian border, and operated by Agip since then. Ashtart (production around 15,000 bbl/d) is the only other oilfield with proven and estimated reserves over 100 million barrels. About 75% of Tunisian oil production comes from these two fields and the Sidi El Kilani field. However, production at all three fields has been declining steadily. The Al Manzah field started production at 4,000 bbl/d in October 2000, with Centurion of Canada the operator.

As of December 2002, ETAP reportedly was awaiting tenders on 20 blocks, including onshore blocks C1-C4 (central Tunisia) and S1-S5 (south Tunisia), plus offshore blocks N1-N4 (northern Tunisia) and E1-E7 (eastern Tunisia). Fields currently under development include Isis, al Manzah, Belli, and Ashtart. In addition, there is ongoing work at the following blocks and permit areas: Grombalia, Kerkouane, Jenein North, Chorbane, Borj el Khadra, Baraka South, Kebili, El Hamra, Bazma, Jorf, Fejaj, Anaguid, Mellita, Robbana, Alyane, Tatouine, and North Kairouan. Companies involved include Agip, Anadarko, Anschutz, Centurion, Coparex Netherlands, Eni, Eurogas, Kufpec, Lasmo, Nuevo, Petro-Canada, and Preussag.

Tunisia has five oil terminals on the Mediterranean coast. The largest of these is La Skhirra, on the Gulf of Gabes. A 22,000-bbl/d, 78-mile pipeline between the Sidi El Kilani oilfield and La Skhirra was inaugurated in March, 2001. In addition, a line from Algeria carries oil from that country's southern, In Amenas region, for export. Other Tunisian oil terminals include Ashtart, Gabes, Sfax, and Bizerte. In addition, anew terminal at Bejaia (140 miles east of Algiers), with the capacity to accommodate crude tankers as large as 300,000 tons, is scheduled to be constructed by late 2003 or early 2004.

Natural Gas

Tunisia has 2.8 trillion cubic feet

(Tcf) of proven natural gas reserves, with around two-thirds located

offshore. In 2000, Tunisia produced 66 billion cubic feet (Bcf) of natural

gas. The majority of the country's gas output comes from the 1-Tcf Miskar

non-associated gas field, discovered in 1975 by Elf and now operated by

BG, in the offshore Amilcar permit. Tunisia has four other small producing

natural gas fields (El Franning, El Borma, Baguel, and Zinnia) that

together produced almost all of the remainder of domestic production. In

general, the Tunisian natural gas sector is considered more promising than

the country's oil sector.

BG, the largest investor in Tunisia's energy sector and the operator of the Miskar field, has a tentative agreement to supply a large proportion of Tunisia's domestic gas requirements through 2020. Miskar, located about 80 miles offshore in the Gulf of Gabes, currently produces 205 million cubic feet per day (Mmcf/d) of gas, which supplies around two-thirds of Tunisia's total gas demand. Miskar production is being expanded in several phases over five years at a cost of $120 million, with production expected to peak at 230 Mmcf/d before a decline sets in around 2009.

Besides Miskar, BG is planning on developing the Hasdrubal natural gas and gas condensate field, also located in the Gulf of Gabes, at a cost of $330 million over a 12-year period. In August 2002, BG announced that it had found oil at the Hasdrubal South West-1 field. The Tunisian government has decided to delay production from the Hasdrubal field until 2007, in advance of the decline of the Miskar field. BG is conducting exploration and is considering development of the Jugutha gas field. Finally, BG is looking at developing compressed natural gas as a vehicle fuel, especially for public transport, in Tunisia.

The 850-Bcf-per-year-capacity Trans-Mediterranean (TransMed) pipeline transports Algerian natural gas to Sicily, crossing the Mediterranean seabed from Cap Bon. Tunisia receives royalties (5.25%-6.75% of the gas' value, in cash or in kind) from this pipeline as payment for access through its territory. A natural gas pipeline also is set to link Libya and Tunisia, with an agreement signed in 2001.

Electricity

Tunisian power demand is growing

rapidly, at an estimated 7% annually. Recent census figures indicate that

around 94.6% of Tunisian homes had access to electricity in 1999, up

sharply from 85.9% in 1994. Around 95% of Tunisian power generating

capacity is natural-gas fired, with 4% oil-fired and 1% hydroelectric.

Tunisian generating capacity is expected to reach 3,540 MW by 2006, up

from 2,480 MW in early 2002.

The $261-million, 471-megawatt (MW), Rades combined cycle (natural gas and diesel-fired) power project is scheduled to come online shortly. A consortium comprised of U.S.-based PSEG (60%), and Japan's Marubeni (40%) is developing the project on a 20-year build-own-operate-transfer (BOOT) basis. Rades -- Tunisia's first independent power plant -- is to supply 20%-25% of the country's power needs. Tunisia's state-owned gas and power company, STEG (Societe Tunisienne de l'Electricite et du Gaz) has signed a 20-year power-purchase agreement with the consortium building Rades. Under this deal, STEG will by 100% of Rades power output while PSEG manages the facility.

Besides Rades, BG is planning to build a $200-million, 500-MW power plant near Sfax that will utilize natural gas from the Miskar, and eventually, Hasdrubal fields. BG will likely partner with STEG or ETAP, and the facility should be operational in 2006. Also, a 27-MW, gas-fired power plant is being built at Zarsis, next to the El Biban gas field. Previously, El Biban natural gas was flared, but once complete, the power plant will take around 6 million cubic feet per day of El Biban gas as feedstock.

In July 2002, the European Investment Bank (EIB) approved a 150 million Euro loan aimed at upgrading Tunisia's power transmission network. Main elements include high-voltage power lines, underground cables, power transformers, and telecommunications for network control and transmission. Tunisia's power grid is in need of upgrading both to meet domestic demand as well as to increase reliability as part of Tunisia's ongoing integration into Europe's power grid. Currently, Tunisia is connected to Algeria's power grid, and is in the process of being linked to Libya as well.

|

Table 1. Economic and Demographic Indicators for the Arab Maghreb Union | |||||

|---|---|---|---|---|---|

|

Country |

Gross Domestic Product (GDP), 2002E (Billions of U.S.

$) |

Real GDP Growth Rate, 2002 Estimate |

Real GDP Growth Rate, 2003 Projection |

Per Capita GDP, 2002E |

Population |

| Algeria |

$55.1 |

3.4% |

4.3% |

$1,762 |

32.3 |

| Libya |

$16.6 |

1.8% |

2.9% |

$3,001 |

5.4 |

| Mauritania |

$1.0 |

3.7% |

4.5% |

$343 |

2.8 |

| Morocco |

$36.6 |

3.8% |

4.3% |

$1,235 |

31.2 |

| Tunisia |

$21.1 |

2.0% |

4.3% |

$2,155 |

9.8 |

| Regional Total/Average |

$130.4 |

3.1% |

4.1% |

$1,600 |

81.5 |

|

Table 2. Energy Consumption and

Carbon Dioxide Emissions in the Arab Maghreb Union, 2000 | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Country | Total Energy Consumption (Quadrillion btu) | Petroleum | Natural Gas | Coal | Nuclear | Hydro- Electric | Other Renewable Electric | Net Electricity Imports | Carbon Dioxide Emissions (Million metric tons of carbon) |

| Algeria | 1.23 | 31.9% | 66.5 | 1.7 | 0.0 | 0.0 | 0.0 | 0.0 | 22.7 |

| Libya | 0.58 | 66.1% | 33.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 10.9 |

| Mauritania | 0.05 | 100% | 0.0 | 0.0 | 0.0 | 0.5 | 0.0 | 0.0 | 0.9 |

| Morocco | 0.42 | 72.4% | 0.4 | 21.3 | 0.0 | 3.1 | 0.0 | 0.0 | 7.8 |

| Tunisia | 0.29 | 57.0% | 42.9 | 0.0 | 0.0 | 0.4 | 0.0 | 0.0 | 5.2 |

|

Regional |

2.57 | 50.3% | 44.2 | 4.3 | 0.0 | 0.6 | 0.0 | 0.0 | 4.5 |

Note: percentages may not add up to 100% due to rounding.

|

Table 3. Energy Supply Indicators,

Arab Maghreb Union | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Country | Crude Oil Reserves, 1/1/03 (Million Barrels) | Natural Gas Reserves, 1/1/03 (Billion Cubic Feet), | Coal Reserves (Million Short Tons) | Petroleum Production, 2002E (Thousand Barrels Per Day) | Natural Gas Production, 2000 (Million Short Tons) | Coal Production, 2000 (Million Short Tons) | Electric Generating Capacity, 2000 (Gigawatts) | Crude Oil Refining Capacity, 1/1/03 (Thousand Barrels Per Day) | |

| Algeria | 9,200 | 159,700 | 44 | 1,460 | 2.9 | 0.02 | 6.0 | 450 | |

| Libya | 29,500 | 46,400 | 0 | 1,377 | 0.2 | 0.0 | 4.6 | 343 | |

| Mauritania | 0 | 0 | 0 | 0 | 0 | 0.5 | 0.1 | 0 | |

| Morocco | 1.6 | 43 | 6 | 1.5 | 0 | 3.1 | 4.1 | 155 | |

| Tunisia | 308 | 2,750 | 42.9 | 78 | 0.1 | 0.4 | 2.0 | 34 | |

|

Regional |

39,010 | 208,893 | 50 | 2,916.5 | 3.2 | 0.6 | 16.8 | 982 | |

Sources for this report include: Africa Energy Intelligence; Africa News; Africa Oil and Gas Bulletin; Africa Research Bulletin, AFX.COM, The Age (Melbourne); AP Worldstream; APS Review Gas Market Trends; APS Review Oil Market Trends; The Australian; Business Wire; CIA World Factbook 2002; CWC Africa Energy Alert; Dow Jones International; Economist Intelligence Unit; Energy Day; Europe Information Service; Financial Times; Middle East Economic Digest (MEED); Middle East Economic Survey (MEES); Middle East Executive Reports; Middle East News Online; Oil and Gas Journal; Petroleum Economist; Petroleum Intelligence Weekly; PR Newswire; U.S. Energy Information Administration; Weekly Petroleum Argus; World Gas Intelligence; World Markets Online.

LINKS

For more information from EIA on Mauritania, Morocco, and Tunisia, please see:

EIA: Country Information on Mauritania

EIA: Country Information on Morocco

EIA: Country Information on Tunisia

Links to other U.S. government sites:

U.S. Agency for International Development

CIA

World Factbook 2002

Library of Congress --

Mauritania Country Study

U.S. State Department

Consular Information Sheet on Mauritania

U.S. State

Department Background Notes on Mauritania

U.S.

Department of Energy's Office of Fossil Energy's International section -

Morocco

U.S. State

Department's Consular Information Sheet - Morocco

U.S.

State Department Country Economic Report

U.S.

Commercial Service -- 1999 Country Commercial Guide

U.S. Embassy in Morocco

U.S.

Department of Energy's Office of Fossil Energy's International section -

Tunisia

U.S. State

Department's Consular Information Sheet - Tunisia

U.S.

State Department Country Economic Report

U.S. Embassy in

Tunisia

The following links are provided solely as a service to

our customers, and therefore should not be construed as advocating or

reflecting any position of the Energy Information Administration (EIA) or

the United States Government. In addition, EIA does not guarantee the

content or accuracy of any information presented in linked sites.

MENA

Petroleum Bulletin

AME Info

Middle East Business Information

Planet Arabia.com

Mauritania

Embassy in the United States

University

of Texas at Austin: Mauritania information page

University

of Pennsylvania: Mauritania information page

Columbia

University: Mauritania information page

Official Mauritanian Government News

Agency

American Chamber of

Commerce in Morocco

Arab

Net page on Morocco

University of

Texas at Austin Center for Middle Eastern Studies - Morocco

Washington

Post Morocco page

Arab World Online --

Morocco

Mbendi -- Morocco

Oil Industry Profile

Enterprises

Tunisienne d'Activites Petrolieres (ETAP)

Arab Net page on Tunisia

University of

Texas at Austin Center for Middle Eastern Studies - Tunisia

University

of Pennsylvania African Studies - Tunisia

Washington

Post Tunisia page

Mbendi

-- Tunisia Oil Industry Profile

Africa News Online -

Tunisia

British Gas

in Tunisia

If you liked this Country Analysis Brief or any of our many other Country Analysis Briefs, you can be automatically notified via e-mail of updates. You can also join any of our several mailing lists by selecting the listserv to which you would like to be subscribed. The main URL for listserv signup is http://www.eia.doe.gov/listserv_signup.html. Please follow the directions given. You will then be notified within an hour of any updates to Country Analysis Briefs in your area of interest.

Return to Country Analysis Briefs home page

File Last Modified: January 16, 2003

Contact: Lowell Feld

lowell.feld@eia.doe.gov

Phone: (202) 586-9502

Fax: (202) 586-9753