|

Theme: The extraordinary increase in oil exploration

in the area between Spain and the Maghreb highlights the risks

associated with the lack of bilateral delimitation treaties

with Morocco and Algeria.

Summary: Two years ago there were no companies

exploring for oil in Spanish waters bordering on, or near,

Moroccan waters. Today, five oil companies are operating along

the Spanish/Moroccan maritime border in three different areas:

the Atlantic side of Gibraltar, the Alboran Sea and the coast

of the Canary Islands. In two cases, the same company holds

exploration rights on both sides of the maritime limit. This

unusual activity has awakened the interest of the Algerian

government, which has called for tenders for the exploration

of what it considers its territorial waters in East Alboran,

directly on the north-south line with La Manga del Mar Menor.

This includes an area that has traditionally been considered

to belong to Spain.

The large rise in exploration very substantially increases

the likelihood of hydrocarbons being found in at least one of

these zones and also, that extracting them will be

economically viable. In this case, Spain will be faced with

one of the most delicate and complex issues in international

relations: delimiting maritime jurisdictions where hydrocarbon

deposits lie beneath the seabed, something that has led, with

alarming frequency, to conflicts of varying intensity.

Analysis: Repsol takes control of the Atlantic

side of Gibraltar

The Spanish oil company Repsol YPF has recently obtained

permission to explore three zones along the Atlantic coast of

Morocco, from Tangiers south to Larache. The area covers 6,000

km2 (about the size of the province of Gerona),

which the company will explore for eight years. This agreement

is similar to another dozen that Morocco has signed with other

oil companies. The particularity of this agreement is that it

affects Moroccan waters bordering on Spanish ones. Also, it

turns out that Repsol also holds exploration rights on the

Spanish side, off the province of Cadiz, where it has seven

exploration licences adjacent to those it has just received

from Morocco.

To

determine Repsols possible interest in the Tangiers-Larache

zone, it must be kept in mind that in January 2002 Repsol

received nine licences from the Spanish government for

hydrocarbon exploration between the coast of Morocco and the

islands of Lanzarote and Fuerteventura. Rabat reacted harshly

to this concession, sending the Spanish embassy a diplomatic

note that labelled this action as unfriendly and

unacceptable. The Moroccan Foreign Minister, Mr Benaissa,

claimed that Spain had unilaterally determined the limit

between the areas of interest off the Canary Islands and

Morocco. The note ended insistently inviting Spain to suspend

its application (see Petróleo: ¿el próximo conflicto

hispanomarroquí?, by Íñigo Moré,

http://www.realinstitutoelcano.org/analisis/60.asp). It

is true that the Moroccan protest made no reference to Repsol.

However, it can also be assumed that it in no way motivated

Repsol executives to visit Rabat. To

determine Repsols possible interest in the Tangiers-Larache

zone, it must be kept in mind that in January 2002 Repsol

received nine licences from the Spanish government for

hydrocarbon exploration between the coast of Morocco and the

islands of Lanzarote and Fuerteventura. Rabat reacted harshly

to this concession, sending the Spanish embassy a diplomatic

note that labelled this action as unfriendly and

unacceptable. The Moroccan Foreign Minister, Mr Benaissa,

claimed that Spain had unilaterally determined the limit

between the areas of interest off the Canary Islands and

Morocco. The note ended insistently inviting Spain to suspend

its application (see Petróleo: ¿el próximo conflicto

hispanomarroquí?, by Íñigo Moré,

http://www.realinstitutoelcano.org/analisis/60.asp). It

is true that the Moroccan protest made no reference to Repsol.

However, it can also be assumed that it in no way motivated

Repsol executives to visit Rabat.

Given these precedents, the only reasonable conclusion is

that Repsol approached Morocco with a clear goal in mind and

weighty arguments to back it up. These arguments are the seven

oil concessions that Repsol operates on the Spanish side of

the Atlantic coast of Gibraltar. All together, these licences

located on the Spanish side of Gibraltar come to 275,410

hectares or 2,754 km2 (larger than the province of

Vizcaya). More importantly, these concessions are the most

fertile in Spain: 90% of domestic natural gas is extracted

from them.

Repsol acquired the Poseidón Norte and Poseidón Sur

concessions in 1995. Both are located in open seas 30 km south

of Huelva. These concessions turned out to be the most

successful ever drilled on the Spanish coast and in 2002

produced 503 million m3 of gas. This volume

represented 90% of all the gas extracted that year in

Spain.

In light of this success, Repsol continued southward along

the coast. In 1997, it requested the Hércules Norte and Sur

maritime concessions, adjacent to Poseidón, but in the

province of Cádiz. These zones turned out to be sterile, so in

2001 Repsol continued southward and in December acquired the

Calypso Este and Oeste, on the maritime perimeters. These are

adjoining and centred on the Bay of Cádiz. Both licences form

a rectangle whose short side runs north to south,

approximately from Chipiona to Conil. Repsol immediately began

preliminary work, which according to the terms of the

concession includes 3-dimensional seismic studies of an area

of 600 km2, geochemical studies and others, all

worth a total of at least 4.1 million.

The company must have found something interesting because

on March 21, 2003, it was able to sell the German company RWE

Dea AG 25% of the perimeters, with an option to acquire up to

30%. This means that the German company will take on part of

the investment, but only as a minority shareholder, remaining

subordinate to the Spanish companys management decisions.

The consortium immediately drilled appraisal well CO-1 on

the Calypso Oeste licence. It finished drilling on April 27,

having reached a depth of 1,900 m. The next day, April 28, it

began appraisal well CO-2, set to reach a depth of 1,900 m.

One day after finishing this, drilling was begun on CE-1, on

the Calypso Este licence. Like the others, 1,900 m was the

targeted depth.

Repsol has not provided any information on the results of

these tests, but they would seem to be positive, perhaps even

very positive. On May 30, 2003, the company obtained the Circe

licence, which implies extending Calypso to the west. This

suggests that wells CO-1 and CO-2 indicate the existence of

reserves extending to the adjacent zone.

This set of activities by Repsol in the zone suggests that

the company was hoping the success of Poseidón could be

extended to the south, first with the Hércules licences, then

with Calypso and finally with Circe. The Olympian origin of

the names of the concessions suggests that Repsol considers

them part of the same group and, therefore, of a similar

geology. Also, the Olympian connotations clearly suggest the

magnitude of Repsols expectations, already confirmed in the

case of Poseidón, the main Spanish gas reservoir. As part of

this strategy , it seems logical for Repsol to study the

adjacent zone to the south; in other words, to apply to

Morocco for concessions. This is not to rule out the

possibility that these reservoirs could also extend to

Portugal, where Repsol YPF is already operating (Offshore

Algarve, Portugal: A Prospective Extension of the Spanish Gulf

of Cadiz Miocene Play, by J. Cakebread-Brown, C.

Garcia-Mojonero, R. Bortz, L. Cortes, W. Schwarzhans and W.

Martínez del Olmo).

From the Moroccan point of view, it also seems natural to

grant the oil concession for its north shore to the company

already operating on the Spanish side. Repsol has inestimable

experience in the zone, knows its geology and has explored it

successfully. This guarantees that the Spanish company has a

precise idea of what could lie below the seabed on the north

coast of Morocco, putting it in the best position to find

hydrocarbons, if any are to be found. This argument could be

solid enough to eclipse other issues, particularly Moroccos

dramatic interpretation of the Repsol concessions between the

Canary Islands and Morocco.

The Canary Islands and Morocco The coast of the Canary

Islands has been studied by Repsol since the company received

nine adjacent concessions between the Canary Islands and

Morocco. Under the terms of the concession, Repsol was obliged

to invest 10 million in two and three-dimensional geological,

geochemical and seismic-stratigraphic studies. These studies

have already been carried out and are reason for some

optimism. They have been sufficient to lead the Australian

company Woodside to buy 30% of the concessions from Repsol in

2003, while the German company RWE Dea AG bought another 20%.

Both companies will cover their share of the costs, while

accepting Repsols management decisions. Woodsides

participation is very significant, since it is the main

foreign operator on the coast of Mauritania, where it has five

concessions along the central coast of the country. It has

drilled three wells there, locating significant amounts of oil

(Chinguetti-1, Chinguetti-4-2 and Chinguetti-4-3), leading to

hopes for the first hydrocarbon operation in Mauritanian

waters. To date, the Australian company is the only one that

has been successful on the Mauritanian coast and its entry

into the Repsol consortium could be interpreted as the result

of speculation that the Mauritanian reservoir could extend

northward. Much more important is the fact that the entry of

these two companies into the consortium led by Repsol backs

the legitimacy of the concessions, which Morocco has

questioned with unusual harshness. In the early months of

2004, Repsol will drill its first well in the zone. To

the south of this concession, on the shores of the Sahara, are

the controversial concessions granted by Morocco in 2001,

dividing the Saharan coast between the US company Kerr Macgee

and TotalFina. Since then, Rabat has been annually renewing

this reconnaissance licence which does not grant drilling

rights. Responding to these concessions, the Polisario

Front contracted the Australian company Fusion Oil to assess

Saharan oil resources. This small Australian company has sold

an option to 35% of its technical assistance contract with

the RASD to Premier Oil, a British oil company. The agreement

forces Fusion to provide a free report on oil prospects on the

Saharan coast. As remuneration, it has received a promise of

three oil concessions in the zone, each one up to 20,000

km2, once the Sahara becomes independent. The

modest Australian company was once thought to believe that the

future of the Sahara would take the same course as that of

East Timor, near Australia. It now appears that a much larger

British company with significantly greater experience shares

its vision. To make use of its option, Premier Oil will pay

70% of the costs already incurred, taking 35% of any

concession that Fusion may acquire. It must be kept in mind

that this transaction is part of a general association

through which the British company has taken stakes in its

Australian counterparts concessions on several occasions.

In early October, two representatives of Fusion and

Premier presented the technical study to the Polisario at a

formal event. Fusion claims that it provides reasons for

cautious optimism on the oil geology of the zone. Premier

Oil, for its part, says that regional studies undertaken by

Premier and Fusion indicate that the area has exciting oil

potential. Fusion has announced that in November it will

request that the Polisario grant three drilling licences,

though it says that concession of these will have to be

ratified by the UN. It seems, therefore, that the

Polisario has increased support for its pretensions in the

zone, though this will not likely be enough for the conflict

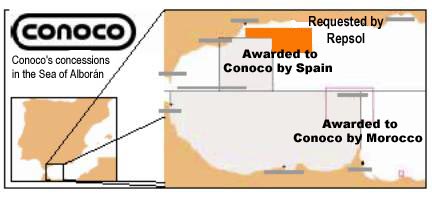

to be resolved in its favour. Repsol puts Alborán under

Spanish influence and awakens Algerian interest This unusual

interest in the limits between Spain and the Maghreb

heightened with Repsols arrival in the Alboran Sea, an area

where the US company Conoco operates. This company holds

negotiating rights to a research contract that covers the

Moroccan side of Alborán, though its concept of territorial

waters is very broad, since it apparently covers waters that

surround Ceuta, Melilla and even the island of Alborán itself

(see Petróleo: ¿el próximo conflicto hispanomarroquí?, by

Iñigo Moré,

http://www.realinstitutoelcano.org/analisis/60.asp). In a

demonstration of fair play, in 2001 Spain granted this company

oil rights in the Spanish part of Alborán, near the province

of Malaga. However, last July, Repsol applied for Siroco A, B

and C licenses, all adjacent to one another and located in the

Alboran Sea in line with the province of Malaga. These three

concessions surround those held by Conoco in Spanish waters,

literally blocking off its concessions on the northwest side.

Although there is healthy competition in the Spanish

hydrocarbon exploration sector, there have been a few cases of

similar actions, in which one company requests the perimeter

surrounding another. Obviously, this means that Repsol

considers it likely that there are hydrocarbons in the same

zone that Conoco does. Also, this movement could be considered

unfriendly since it partially closes the American companys

access to land. This could cause operational difficulties to

Conoco, though it adds a Spanish presence to a situation in

which the American company was benefiting from a monopoly in

the Alboran Sea.

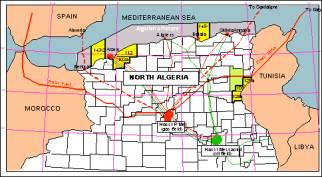

In light of all this interest, Algeria has played its ace

by calling for tenders for oil exploration in what it

considers its territorial waters on a north-south line between

Oran and Cartagena. In the framework of the fourth round of

oil concessions, which will close on December 1 of this year,

Algeria has invited tenders for exploration zones in 12 areas

of the country, with different blocks. Among the most

important of these are 143-2 and 145-1, both located along the

Algerian shore. 143-2 makes a 8,794 km2 rectangle

at the easternmost end of the Alboran Sea, ending opposite

what would be Spanish territorial waters. The other marine

block, 145-1, covers 6,924 km2 along the Algerian

shoreline near Bejaia, approximately on the 5º E parallel,

south of Minorca. In this case, the end of the block is about

200 km from Minorca and also facing Spanish waters. Both

blocks are shown in yellow on the following map prepared by

Sonatrach.

For the moment, the Algerian coast has hardly received

attention and has only been drilled on two occasions (see

The Petroleum Prospectivity of the Deep-Water Margin of

Algeria, by Michael J. Cope). So

far, Sonatrach had preserved its coastline, which was shown on

maps of the Algerian mining domain as a research zone

reserved for the state-owned company. This research has

consisted of a geological study of the seabed, which in the

Cartagena-Oran corridor reaches depths of up to 2 km. The fact

that Sonatrach has invited tenders for the zone could mean

that it has found reasonable signs of the presence of

hydrocarbons. This likelihood is proportional to Sonatrachs

capacities: as the 11th biggest oil company in the

world, its technical expertise must be very high. Also, with a

business volume of US$18.1 billion in 2002, Sonatrach is

Africas main business group, the worlds second largest

exporter of LNG and the third largest exporter of natural

gas. So

far, Sonatrach had preserved its coastline, which was shown on

maps of the Algerian mining domain as a research zone

reserved for the state-owned company. This research has

consisted of a geological study of the seabed, which in the

Cartagena-Oran corridor reaches depths of up to 2 km. The fact

that Sonatrach has invited tenders for the zone could mean

that it has found reasonable signs of the presence of

hydrocarbons. This likelihood is proportional to Sonatrachs

capacities: as the 11th biggest oil company in the

world, its technical expertise must be very high. Also, with a

business volume of US$18.1 billion in 2002, Sonatrach is

Africas main business group, the worlds second largest

exporter of LNG and the third largest exporter of natural

gas.

This is not bad news for Spain, since geology knows no

political boundaries and the same signs could extend into

Spanish waters. Spain could thus reduce its energy dependence

on Algeria (see España profundiza su dependencia energética

de Argelia, by Iñigo Moré, http://www.realinstitutoelcano.org/analisis/86.asp).

Finally, it must be noted that Algeria is not the only

party interested in Spanish hydrocarbons. In 2003, the

prestigious American Association of Petroleum Geologists held

its international conference in Barcelona. In nearly two

hundred presentations, it exhaustively studied Spains oil

potential, and specifically regional geology at the main

session of the conference.

Risks and opportunities It must be emphasized that the

existence of hydrocarbons has not been proven in any of the

three zones, though there are well-founded hopes based on

previous experiences such as Poseidón and the exploration on

the Mauritanian coast. Even in the absence of these

precedents, the large amount of exploration on the limits

between Spain and the Mahgreb substantially raises the

likelihood of finding hydrocarbons at one or more of these

sites. If hydrocarbons are found, and if they spread

across both jurisdictions, negotiations on the exploitation of

the resources located would begin between the holders of

rights on either side. The problem is that Spain would start

off on the worst possible footing in this process, since it

has not signed any treaties delimiting its maritime boundaries

with Morocco or Algeria which, as we have seen, do not always

seem to coincide. Spain, meanwhile, has signed this kind of

treaties with countries as unlikely as Italy. Spain has tried

to compensate for this situation by having one of the working

groups created to re-launch Spanish/Moroccan relations focus

on this issue. The group, however, limits its activities to

maritime boundaries in the Canary Islands area. To date, there

has been no public announcement of any agreement, though it

does seem clear that the parties have the will to reach points

of agreement. At least, Rabat has not repeated its protest.

One expression of this goodwill is the successive awards of

concessions to Repsol in Gibraltar-Atlántico. On the

other hand, these concessions are almost obligatory, given the

record of the Spanish oil company in the zone, and the special

circumstances of their location. The limit between Spanish and

Moroccan jurisdiction on the Atlantic side of Gibraltar

coincides with the narrowest point in the Strait, where heavy

sea-going traffic would make the installation of oil rigs

unadvisable, even if hydrocarbons were to be found there.

Although modern technology makes it possible to face all kinds

of technical difficulties, deposits in the Strait, right in

front of Gibraltar, would likely present insurmountable

obstacles. Considering that Repsol is the title-holder on both

sides and that deposits in the middle would be more difficult

than attractive, the zone would seem to present little

potential for conflict in this respect. The situation

on the Saharan coast is more complex, since in addition to the

problem of there being no delimitation of waters, there is the

well-known dispute over the regions sovereignty. On this

issue, two oil companies have accepted Rabats arguments and

two others have sided with the Polisario Front. After several

years of investigation, those working for the Polisario have

now completed their preliminary studies; this is most likely

also the case of those working in Morocco. All of them have no

doubt defined their goals in the zone and are technically

prepared to move on to the drilling stage. The areas low

level of economic development and its energy dependence are an

incentive for this. However, the companies working with the

Polisario lack the economic resources to undertake activities

on their own. In June 2003, Fusion Oil had assets of only

AUS$16.2 million, while at the end of 2002, Premier Oil had

assets of £101 million. By contrast, the companies with

licences in Morocco are international giants with more than

sufficient economic capacity. A unilateral decision to drill

would cause tensions that could affect Spain; especially

considering that the southern limit of the Canary Islands

jurisdiction would be adjacent to the Sahara, to say nothing

of its effect in the general context of the Saharan conflict.

In this area, it seems that an orderly exploitation of

the eventual riches of the zone, in accordance with

international law, is in the interests only of Spain.

The case of the Moroccan and Algerian sides of the Alboran Sea

involves other considerations. Repsols arrival, surrounding

Conoco in the zone, would seem to end the monopoly that the US

company has enjoyed until now. Since the areas requested by

Repsol in the zone are far from the Spanish/Moroccan limit,

this situation is unlikely to lead to any immediate tensions,

unless the companys endorsement of Conocos strategy arouses

Moroccan interest in the zone. It must be borne in mind that

Rabat has negotiated a reconnaissance contract with Conoco

that affects the entire Mediterranean shore of Morocco, in a

broad interpretation of its jurisdiction in the zone. At any

time, Rabat could raise this contract to an exploration

licence to allow drilling. For its part, Algeria could

contribute to arousing this interest with its decision to

invite tenders for the exploration of two maritime zones,

especially the one located in East Alboran, on the

Cartagena/Oran line. It is important to highlight that the

Algerian decision implies the delimitation of its jurisdiction

in the zone: it sets the northern limit at 36º 55 latitude

and 0º 30 W longitude, approximately in line with La Manga

del Mar Menor. A superficial analysis does not necessarily

lead to the conclusion that this point corresponds to the

natural line between the two countries. At this longitude,

Spain ends at Cabo de Palos at 37º 37 latitude, while the

extreme north of Algeria at that longitude is approximately

35º 55. The mid-point, therefore, would be about 10 to the

south of where Algeria sets the limit of this block. For the

moment, the Spanish Ministry of Foreign Affairs has not

reacted publicly, which does not mean it has accepted this.

Technically, it would be necessary for Algeria to officially

grant exploitation rights to the zone to a specific company.

This may never happen. Given the current good relations

between Madrid and Algiers, the most likely cause of this

situation could be a simple cartographic error a situation

also influenced by a lack of care on the part of Spain, which

does not have an official map of what are, or what it

considers to be, its waters. This situation could well be

solved by a simple conversation. It is significant that Spain,

in late 2001, made the strategic decision to strengthen its

already close energy relations with Algeria. This country is

Spains main energy supplier, providing 15% of the total.

Thanks to this decision, this could reach 30% by 2010 (see

España profundiza su dependencia energética de Algeria, by

Iñigo Moré,

http://www.realinstitutoelcano.org/analisis/86.asp).

Apart from territorial questions, and whether or not there are

hydrocarbons in the zone, the proximity of the Algerian and

Moroccan coasts could lead to environmental problems,

aggravated by the fact that opposite some of the exploration

zones there are tourist centres such as La Manga del Mar

Menor, the Costa del Sol and the coast of Cádiz. Such

environmental risk is almost non-existent in Spain thanks to

strict regulations. Before drilling, oil companies must inform

the Ministry of the Environment of their plans, opening a

transparent process of public consultation before any

authorization is granted. In this way, problems can be avoided

which could otherwise be irreparable. However, in countries

such as Algeria and Morocco environmental questions are not

given the priority they receive in Spain and their

environmental regulations are nominal compared to Spains,

which applies European standards. Without doubt, Repsol will

operate in Tangiers-Larache with the same diligence as in

Cadiz, but it is impossible to know who will obtain the

Algerian licence across from La Manga or if environmental

commitment will be included in their corporate mission

statement.

Conclusions: All this encourages the Spanish

government to continue its efforts to delimit jurisdictions

with Morocco and to extend this process to Algeria. This will

not always be up to Madrid to decide, since it takes two to

tango. For this reason, it could be useful to establish one or

more Spanish-Mahgreb institutional forums on environmental and

oil-related issues. It would even be interesting to broaden

their scope of action to energy issues in general, given the

electrical connections and gas lines between Spain and the

Maghreb. These institutions would enable information to be

shared and would serve as a basis for purely technical

initiatives such as training or professional practices. They

would even serve to coordinate efforts in emergency

situations. A possible model is the group of cross-border

institutions between the US and Mexico, such as the US-Mexico

Environment Commission or the US-Mexico Border Health

Commission (see El escalón económico entre vecinos. El caso

España-Morocco, by Íñigo Moré,

http://www.realinstitutoelcano.org/documentos/44.asp).

Iñigo Moré

Consultora Mercados Emergentes

mercadosemergentes@hotmail.com |

Print

Print Send

Send Statistics

Statistics